When you have expensive or otherwise valuable jewelry, it deserves to be protected with the right coverage. The limits of your homeowners insurance might not be enough to fully protect jewelry, especially if you have a lot of it. That's why you might need additional standalone jewelry coverage.

Fortunately, an independent insurance agent can help you find all the jewelry insurance you need. They'll make sure each piece you have gets the appropriate amount of coverage. But first, here's a breakdown of jewelry insurance, when you need it, and more.

Key Takeaways - Jewelry Insurance

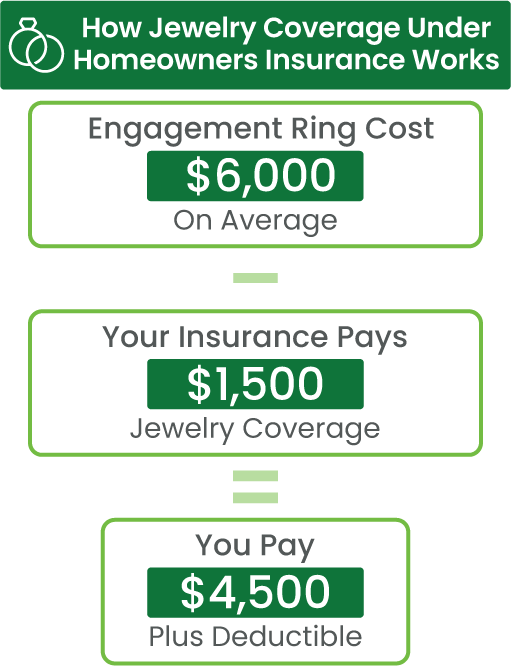

- Homeowners insurance typically caps theft coverage for jewelry at $1,500, which may not be enough for valuable pieces.

- You can add more jewelry coverage to home insurance through scheduling specific pieces, or adding riders, endorsements, or floaters to your policy.

- Standalone jewelry insurance policies can help you cover valuable pieces for their full replacement value.

- You may want separate jewelry insurance if you have a lot of valuable pieces or don't want to increase your home insurance policy's premiums.

- It's highly recommended to work with a local independent insurance agent, as they can shop and compare policies and quotes from multiple insurers and tailor coverage to your unique jewelry.

What Is Jewelry Insurance?

Jewelry insurance is a policy designed to cover your jewelry against various threats, including theft, mysterious disappearance, and damage or destruction caused by elements such as fire. In exchange for the premiums you pay, your insurance carrier will reimburse your financial losses or even replace the item up to its specified value.

Does Homeowners Insurance Cover Jewelry?

Yes, jewelry is covered by homeowners insurance, but only to an extent. Coverage for jewelry under your homeowners policy is limited to only a small number of causes, like theft, and has a cap of $1,500. You'll need an additional policy or endorsement to ensure you’re covered for the full value of a piece of jewelry or multiple pieces together.

A more comprehensive option is to "schedule" personal property coverage. This covers a wider range of risks and generally covers the full value of higher-priced items that exceed the regular policy's limit. The scheduling process involves listing each specific item to be covered, along with its value, which is determined by an appraisal.

When and How Does Homeowners Insurance Cover Jewelry?

A standard homeowners insurance policy provides jewelry coverage in a few scenarios. Jewelry falls under the personal property category of homeowners insurance, and it’s treated the same way as many other items under the policy, with one major difference: jewelry has its own special coverage limit under your personal property category.

Example scenarios of when homeowners insurance covers jewelry:

- Someone breaks into your house and steals your jewelry.

- Your jewelry is destroyed or lost due to a covered natural disaster, such as:

- Windstorms

- Hail

- Fires

- Blizzards

Your home insurance policy typically won't cover damage or destruction to jewelry caused by natural flooding, earthquakes, or mudslides. You'll also want to review your specific home insurance policy with your independent insurance agent to determine if you have named perils or all-risk coverage. Named perils coverage will only cover the perils listed on your policy, while all-risk coverage will cover everything except for specific perils listed.

Why You Might Need Additional Jewelry Insurance

Your jewelry will be covered up to your homeowners policy’s limit for the jewelry category under personal property, but your jewelry might easily exceed that, especially if it’s lumped in with other property you need to get reimbursed for at the same time. Consider looking into special jewelry floaters for valuable pieces. Having this extra, specialized coverage will help you get reimbursed for the jewelry’s full value, so you don’t have to worry about losing money.

Scheduled personal property coverage (jewelry floater)

If you’re worried about protecting your more expensive jewelry, you may want to schedule each separate piece on a jewelry floater. A jewelry floater is a special type of inland marine insurance designed for valuable jewelry.

You’d first have to get your specific pieces appraised by a professional jeweler, then send that appraisal to an independent insurance agent. With the appraisal, the agent would be able to help you get the right coverage for your pieces, probably for their full value.

What Does Jewelry Insurance Cover?

Jewelry insurance covers your valuable pieces at their full declared value, which often surpasses the typical limits included in home insurance. Most people's main concern with jewelry is theft, but jewelry owners are also often worried about losing their valuable pieces.

Jewelry insurance covers the following disasters for all types of jewelry:

- Theft (from break-ins to pickpocketing)

- Mysterious disappearances (e.g., dropping, losing, or misplacing)

- Damage (e.g., a gemstone that’s fallen out of a necklace or an accidentally smashed antique watch)

- Fire destruction and damage

An independent insurance agent can further explain the incidents in which your jewelry would be covered by jewelry insurance.

What's Not Covered by Jewelry Insurance?

Jewelry insurance usually won't cover intentional damage to any of your insured jewelry. These policies are designed to protect against accidental losses and damage. Jewelry insurance also won't cover any of your other personal property.

When to Get Standalone Jewelry Insurance

There are some instances in which getting standalone jewelry insurance can make more sense than adding a rider or endorsement to your homeowners insurance policy, such as the following:

- Your homeowners insurance company doesn't offer scheduled personal property endorsements.

- You want to avoid increasing your homeowners insurance premiums.

If you schedule personal property on your home insurance policy or add a rider or endorsement to your coverage, the cost of your premiums will increase. You might find that getting a separate jewelry insurance policy is more cost-effective. An independent insurance agent can also help you weigh the pros and cons of standalone jewelry insurance vs. home insurance riders or endorsements.

| Buy standalone jewelry insurance if you: | Add your jewelry to your home insurance policy if you: |

|---|---|

| Don’t want to increase your home insurance premiums | Don’t have a lot of valuable pieces |

| Have a lot of valuable pieces | Would get sufficient coverage from scheduling pieces or adding a rider, endorsement, or floater |

| Can’t get riders, endorsements, or floaters from your home insurance company |

How Much Does Jewelry Insurance Cost?

The cost of jewelry insurance depends on the kind and amount of coverage you want, your jewelry's total value, your location, and a few other factors. However, jewelry insurance often costs from 1% to 2% of your jewelry's total value, so a $5,000 diamond ring might only cost $50 annually to insure if you have a policy with a $250 deductible.

You also might want to consider increasing your theft coverage through your home insurance before adding standalone jewelry insurance, which is typically inexpensive. The cost to insure a single piece of jewelry under home insurance is around $1-$2 for every $100 in replacement cost.

Increasing the theft coverage limit on your homeowners insurance from $1,500 to $10,000 would only add about $25 to your premium. If you need to get lots of valuable items scheduled, the cost can quickly add up to thousands or even millions per year, which could make getting standalone jewelry insurance well worth it.

Is Jewelry Insurance Worth the Cost?

If your entire jewelry collection is worth over $1,500 and you're worried about losing it, damaging it, or having it stolen or destroyed, then yes, jewelry insurance is likely worth it. Further, many pieces of jewelry may have both sentimental and monetary value. So, protection could be worth it because the items have meaning for you alone.

If you’re still weighing your decision, it’s best to ask yourself, "How easily can I afford to replace an item or all the items if something happens to them?" If the answer is, “Not very easily,” it might be wise to get jewelry insurance.

How Much Do I Have to Pay if Homeowners Insurance Covers My Jewelry?

After paying your deductible, you’ll be responsible for paying any amount exceeding your homeowners policy’s limit for the jewelry category under personal property coverage. This limit will vary by each specific policy.

If you experience a break-in and many of your belongings are stolen, the value of all that property will add up quickly. You might want to increase your coverage or get special jewelry floaters if you have several highly valuable pieces.

A standard homeowners policy has a deductible that’s typically 1% of the home’s value. So, if your home is worth $300,000, you might have to exceed $3,000 in stolen or damaged personal property before your insurance will start paying.

You could easily lose a lot of money this way. If you have valuable jewelry or other kinds of property you want to be covered, it’s a good idea to work with an experienced independent insurance agent to get a policy with a lower deductible.

How to Insure Your Jewelry

First, you'll want to contact an independent insurance agent. They’ll help walk you through the entire process of getting coverage. But here's a sample of what the process of getting jewelry insurance involves:

- List which jewelry pieces you want to be covered: Have an idea of which jewelry items you want insured for before you look into getting coverage.

- Schedule an appraisal: Every local jeweler probably has expertise in conducting appraisals. Your insurance company will need to know the exact value of your jewelry, so an appraisal is often necessary.

- Fill out the paperwork: Submit the official, verifiable documents from the appraisal to your insurance company when you apply for coverage.

- Choose standalone coverage or a rider: Depending on the total value of all the pieces you want to insure, you can choose to get a separate jewelry insurance policy or add coverage to your home insurance through a rider, endorsement, or floater.

- Call your independent insurance agent: Your agent can help you get set up with the right type of coverage for your unique jewelry.

Though there are a few steps to getting jewelry insurance, it can be well worth the effort when you consider how much your valuables might otherwise cost to repair or replace without coverage. An independent insurance agent can help you find the most affordable jewelry insurance near you.

Replacement Cost Coverage vs. Actual Cash Value

When insuring your jewelry, it's important to understand the difference between replacement cost coverage and actual cash value (ACV) coverage.

- Replacement cost coverage: This will pay to replace your jewelry for its full value, without factoring in depreciation.

- Actual cash value coverage: This will pay to replace your jewelry for its original value minus the cost of depreciation.

Knowing whether you have replacement cost coverage or ACV coverage is also important before you try to file a claim. If your jewelry is especially valuable, you'll likely want to opt for replacement cost coverage. An independent insurance agent can help.

Common Jewelry Insurance Mistakes to Avoid

To reduce the risk of having claims denied or not fully covered by your insurance company, be sure to avoid the following common risks when it comes to jewelry insurance:

- Relying on standard limits: You'll want to ensure that the policy or additional coverage you purchase is enough to sufficiently reimburse you for lost, destroyed, or stolen jewelry. Don't hesitate to increase the coverage limits to your satisfaction.

- Not updating appraisals: It's typically recommended to update jewelry appraisals every two to five years. This can help you get an accurate assessment of your pieces' current value, taking into account common fluctuations in the market prices of gold, silver, gemstones, etc. Failing to update your appraisals can lead to issues if you need to file a claim.

- Underinsuring high-value pieces: Without sufficient coverage for your most expensive jewelry, having insurance likely isn't even worth it. Be sure to work with your independent insurance agent to select the coverage options and limits that fully protect your most valuable jewelry.

- Assuming coverage applies worldwide: It's critical to understand your coverage territory for jewelry insurance or the protection provided through your home insurance policy. Review the terms of your coverage together with your independent insurance agent. If you don't have international coverage, it might be wise to leave certain pieces of jewelry at home when you travel.

Working with a local independent insurance agent is an easy way to avoid these common mistakes when insuring your jewelry.

An Independent Insurance Agent Can Help You Find the Right Jewelry Insurance

Independent insurance agents are experts in finding you the right kind of jewelry insurance and any other type of coverage you need. They can shop and compare policies from many different insurance companies to find the best quotes and coverage. Also, they're available down the road to help you file jewelry insurance claims and update your coverage when necessary.

FAQs About Jewelry Insurance

Does homeowners insurance cover engagement rings?

Yes, homeowners insurance can cover engagement rings to the limits in the jewelry coverage category of your policy. However, this coverage is likely not enough to cover the full value of your ring. You may need to schedule your ring or purchase additional coverage in the form of a jewelry rider or floater to insure the full value.

Is jewelry covered outside the home?

Yes, jewelry theft, damage, and loss are usually covered outside of your home. However, coverage limits may be lower for off-premises theft and other losses.

Do I need an appraisal for my jewelry?

Yes, you typically need to get your jewelry appraised so it can be insured for its true value.

Is jewelry insured if I lose it?

Yes, jewelry insurance usually covers "mysterious disappearance," or the loss of your pieces. However, homeowners insurance policies only provide this coverage if you specifically schedule your jewelry pieces.

Can I insure inherited jewelry?

Yes, you can insure inherited jewelry. However, you'll want to be sure to have each piece appraised so it can be covered for its true value.

Sources

https://www.bankrate.com/insurance/homeowners-insurance/does-home-insurance-cover-jewelry/

https://www.progressive.com/answers/what-does-jewelry-insurance-cover/

https://www.travelers.com/jewelry-insurance

https://noblepack.com/blogs/the-daily-noble-blog/jewelry-appraisal