You need your vehicle to get you where you want to go, and you also need to be protected physically and financially when you drive. That’s where auto insurance comes in. But beyond any minimum mandated coverage, you may be wondering if you should choose comprehensive vs. collision insurance to include in your policy.

Exploring the key differences between the two major types of auto insurance, comprehensive and collision, can help you answer these questions. A local independent insurance agent can also help you build a complete auto insurance policy that includes every type of coverage you need. But first, we'll break down comprehensive vs. collision insurance in 2026 and why you might need each type of coverage.

Key Takeaways - Comprehensive vs. Collision Car Insurance

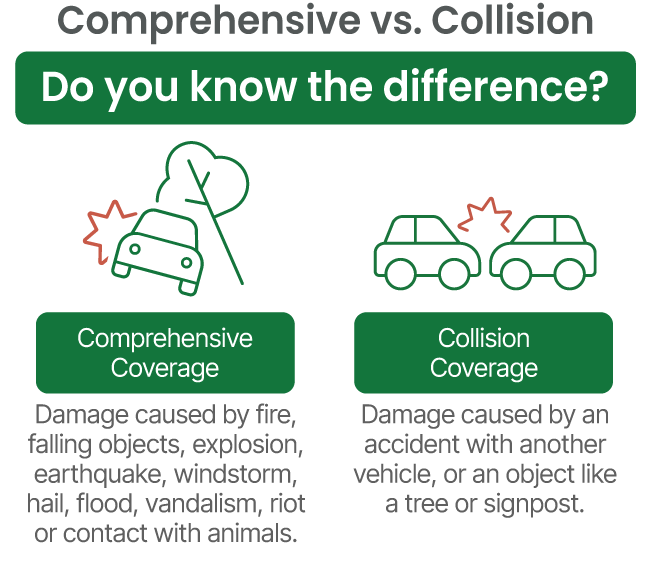

Comprehensive insurance covers vehicle damage caused by events other than collision, such as vandalism, theft, or hail.

Collision insurance covers damage to your car caused by collisions with another vehicle or object.

Both collision and comprehensive coverage may be required by auto lenders and lessors if you have a financed or leased vehicle.

The average cost of collision insurance is $473 per year, while the average cost of comprehensive insurance is $421 per year.

Working with a local independent insurance agent is highly recommended, as they can shop and compare collision and comprehensive quotes and policy options from multiple carriers near you to find the best deal.

Comprehensive vs. Collision: Side-by-Side Comparison

When building your car insurance policy, it's helpful to know what is covered by collision vs. comprehensive insurance, and the cost differences between them. A full coverage car insurance policy includes both collision and comprehensive coverage, in addition to liability insurance. If you've been asking, "Do I need both comprehensive and collision insurance?" the table below can help you decide.

| Comprehensive Insurance | Collision Insurance | |

|---|---|---|

| Covers: | Damage from events other than collision, such as natural disasters, fire, vandalism, falling objects, and large animals. Also covers theft of your vehicle. | Damage caused by collisions with another vehicle or object, such as a fence or signpost. |

| Required by law: | No | No |

| Lender required: | Usually, yes, when you loan or lease a vehicle. | Usually, yes, when you loan or lease a vehicle. |

| Deductible range: | $0 - $1,000+ | $0 - $2,000+ |

| Average annual cost: | $421 | $473 |

What’s the Difference Between Comprehensive and Collision Coverage?

Collision coverage pays for damage to your car when you collide with another object, regardless of fault. These objects could include a fence, guard rail, mailbox, post, or another vehicle. On the other hand, comprehensive insurance, also known as "other than collision" coverage, pays for damage to your car due to non-collision events, such as theft and vandalism.

Both comprehensive and collision coverages go above and beyond the legally mandated minimum liability coverage, which pays for property damage and bodily injury you might cause to other drivers, passengers, or pedestrians.

While collision and comprehensive insurance aren’t required by law, they both offer valuable protection and should be considered when you’re deciding which type of auto insurance to get.

The term “comprehensive coverage” shouldn’t be confused with “full coverage,” which isn't a standard industry term but often is used to refer to an auto policy that includes at least liability, collision, and comprehensive coverage. Comprehensive insurance is only one type of coverage. In some states, comprehensive coverage is called “other than collision” to avoid confusion.

What Is Comprehensive Insurance Coverage?

Comprehensive coverage offers added protection for your vehicle and generally costs less than collision coverage. It can pay to repair or replace your vehicle if the damage wasn't caused by a collision with another car or object.

What comprehensive car insurance covers

- Natural disasters, including earthquakes, hail, lightning, floods, hurricanes, and tornadoes

- Fire

- Riots and vandalism

- Theft

- Falling objects such as trees

- Broken windshields

- Civil disturbance/riot

While comprehensive coverage is commonly called "other than collision," some collisions, such as hitting a large animal, are still covered under this policy. Comprehensive insurance covers hail and other natural-disaster damage, such as damage from lightning or flooding. Also, comprehensive insurance covers vandalism and theft of your vehicle. A local independent insurance agent can help you get set up with comprehensive insurance.

What Is Collision Insurance Coverage?

Collision coverage pays for damage to your car if you hit another vehicle or an object like a telephone pole, a fence, or a mailbox. This coverage applies regardless of fault, meaning that even if the car accident was caused by you, your collision insurance could still cover damage to your own vehicle. Collision coverage reimburses you for the costs of repairing your car, minus the deductible, which is the amount you pay before insurance kicks in.

So, does collision cover hitting a pole? Yes, if you hit an object, such as a telephone pole, with your vehicle, collision coverage can help reimburse you for the damage.

Real-World Examples: When Each Coverage Pays

Perhaps you've been wondering, "Is hitting a deer comprehensive or collision?" The answer is that comprehensive coverage pays for collisions with large animals, including deer. The following table lists several real-world scenarios covered by each type of car insurance.

| Collision Coverage | Comprehensive Coverage |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

How Much Does Comprehensive vs. Collision Coverage Cost in 2026?

The average cost of comprehensive insurance in 2026 is $421 per year, while the average cost of collision insurance is $473. This breaks down to about $35 per month for comprehensive and about $39 per month for collision. Overall, the average cost of car insurance fell by about 6% in 2025, leading to more affordable rates for collision and comprehensive insurance in 2026.

Collision and comprehensive coverage are often purchased together, but you can choose to buy one or both. Generally, comprehensive coverage costs much less than collision.

| Collision Coverage | Comprehensive Coverage | |

|---|---|---|

| Average Annual Cost | $473 | $421 |

Keep in mind that every driver is different, and those costs can vary widely depending on these factors:

- Car value: Expensive cars typically cost more to insure because replacement and repair costs are higher. The opposite is true for cheaper vehicles.

- Safety record: Traffic violations and accidents, particularly major offenses like DUIs, can cause your costs to skyrocket.

- Experience and age: The longer you’ve had your license, the less you’re likely to pay until you hit your senior years. Age is also a factor. Most drivers see a big drop-off in costs after age 25.

- Location: Different regions (called “rating territories”) have different risks that affect costs. For example, drivers in congested cities will likely pay more for insurance because heavy traffic is a risk factor for accidents, even if you’re otherwise a good driver.

To get a better idea of how much an auto insurance policy might cost you, use our car insurance calculator. A local independent insurance agent can also help you compare quotes for affordable coverage in your area.

Average Comprehensive and Collision Cost by State (2026)

The cost of comprehensive and collision insurance can vary greatly depending on where you live. This year, the five most expensive states for comprehensive and collision insurance are Michigan, Washington, D.C., South Dakota, California, and Oklahoma. The three cheapest states are Maryland, Oregon, and Hawaii. Use the table below to find the average annual cost of collision and comprehensive car insurance rates by state for 2026.

| State | Average Annual Comprehensive Cost | Average Annual Collision Cost | Average Annual Combined Cost |

|---|---|---|---|

| Alabama | $307 | $867 | $1,174 |

| Alaska | $230 | $1,047 | $1,277 |

| Arizona | $283 | $803 | $1,086 |

| Arkansas | $606 | $1,206 | $1,812 |

| California | $340 | $1,639 | $1,979 |

| Colorado | $726 | $1,107 | $1,833 |

| Connecticut | $264 | $1,211 | $1,475 |

| Delaware | $283 | $1,115 | $1,398 |

| Florida | $658 | $786 | $1,444 |

| Georgia | $247 | $879 | $1,126 |

| Hawaii | $175 | $842 | $1,017 |

| Idaho | $229 | $867 | $1,096 |

| Illinois | $394 | $870 | $1,264 |

| Indiana | $330 | $890 | $1,220 |

| Iowa | $782 | $994 | $1,776 |

| Kansas | $604 | $1,000 | $1,604 |

| Kentucky | $491 | $934 | $1,424 |

| Louisiana | $556 | $1,217 | $1,773 |

| Maine | $332 | $930 | $1,261 |

| Maryland | $217 | $738 | $955 |

| Massachusetts | $259 | $1,210 | $1,469 |

| Michigan | $667 | $1,613 | $2,280 |

| Minnesota | $562 | $1,086 | $1,648 |

| Mississippi | $477 | $885 | $1,361 |

| Missouri | $587 | $843 | $1,430 |

| Montana | $661 | $908 | $1,569 |

| Nebraska | $572 | $864 | $1,436 |

| Nevada | $297 | $1,032 | $1,329 |

| New Hampshire | $220 | $813 | $1,032 |

| New Jersey | $252 | $1,158 | $1,410 |

| New Mexico | $502 | $1,045 | $1,547 |

| New York | $324 | $711 | $1,036 |

| North Carolina | $383 | $1,434 | $1,818 |

| North Dakota | $619 | $1,138 | $1,757 |

| Ohio | $296 | $831 | $1,127 |

| Oklahoma | $702 | $1,181 | $1,883 |

| Oregon | $218 | $766 | $984 |

| Pennsylvania | $390 | $1,008 | $1,398 |

| Rhode Island | $316 | $1,396 | $1,711 |

| South Carolina | $399 | $759 | $1,158 |

| South Dakota | $1,213 | $806 | $2,019 |

| Tennessee | $464 | $920 | $1,384 |

| Texas | $569 | $1,085 | $1,654 |

| Utah | $174 | $859 | $1,033 |

| Vermont | $333 | $848 | $1,181 |

| Virginia | $227 | $792 | $1,019 |

| Washington | $225 | $978 | $1,203 |

| Washington, D.C. | $524 | $1,640 | $2,164 |

| West Virginia | $591 | $1,027 | $1,618 |

| Wisconsin | $520 | $1,034 | $1,554 |

| Wyoming | $591 | $1,044 | $1,635 |

Average premium by vehicle type (2026)

How much you pay for comprehensive and collision insurance also depends on the type of vehicle you drive. The costs of these specific types of coverage are often the most affected by your vehicle type. However, comprehensive coverage is most affected by a vehicle's theft rate, while collision is most affected by its average repair costs.

Refer to the table below for the difference in average annual full coverage car insurance costs by vehicle type for 2026. These rates are for full coverage auto insurance, which is a policy that includes collision insurance, comprehensive insurance, and liability insurance.

| Vehicle Make and Model | Average Monthly Cost of Full Coverage | Annual Cost of Full Coverage |

|---|---|---|

| BMW 330i | $276 | $3,309 |

| Ford F-150 | $219 | $2,630 |

| Honda Odyssey | $204 | $2,446 |

| Toyota Prius | $231 | $2,774 |

| Tesla Model 3 | $285 | $3,419 |

| Audi Q5 | $257 | $3,088 |

| Toyota RAV4 | $202 | $2,420 |

| Subaru Outback | $187 | $2,242 |

| Jeep Wrangler | $201 | $2,407 |

| Nissan Altima | $244 | $2,934 |

Comprehensive vs. Collision Deductibles: How to Choose

Collision and comprehensive coverages have separate deductibles, and you may be able to choose different deductible amounts for each type. For example, you might adjust your collision deductible based on what you can afford for a collision claim. You can also choose the same deductible for both collision and comprehensive coverage. That way, you’ll have a rough idea of how much you’ll have to pay for all repairs.

The best deductible for car insurance is one you can easily afford if you have to pay it out of pocket when filing a claim. Many people choose $500 deductibles for comprehensive and collision coverage. The average range for a comprehensive deductible is $0-$2,000, while for collision, it's $0-$1,000. Your independent insurance agent can help you choose the right comprehensive vs. collision deductible for your policy.

Comprehensive and Collision Coverage for Leased or Financed Cars

Vehicle lenders and lessors typically require you to have both collision and comprehensive coverage until your auto loan or lease is paid off. Lenders and lessors typically cap your deductible at $500-$1,000.

Having gap insurance can help pay the difference between the amount still owed on a vehicle loan or lease and your vehicle's actual cash value (ACV) if it's declared a total loss. Your independent insurance agent can help you get set up with the right comprehensive and collision insurance on a financed car and review any leased car insurance requirements you need to be aware of.

Do I Need Comprehensive or Collision Coverage?

The type of coverage you need depends on the value of your car, how often you drive it, and whether you can afford to repair or replace it if you have an accident. If you've been asking, "Do I need both comprehensive and collision?", consider the following example scenarios.

- If you’re driving a car that has such a low value that repairs or a replacement would be cheaper than the premiums of additional policies, then you probably don't need more than the minimum mandated liability coverage in your area.

- If you need to choose between comprehensive and collision coverage, base your decision on the way you drive your car. If you commute in heavy traffic, collision coverage is probably the better choice, whereas comprehensive is better in disaster-prone or high-crime areas.

An independent insurance agent can help you choose between comprehensive and collision insurance or add both to your policy. They can also help you weigh buying comprehensive vs. collision for an older car, if you need either coverage at all.

When Should You Drop Comprehensive or Collision Coverage?

If your policy's premiums would exceed a certain amount of your car's value, it's recommended to drop your collision or comprehensive coverage. Consider the 10% rule for car insurance, which states that your collision and comprehensive coverage premiums should be kept below 10% of your vehicle's current ACV.

If your car is worth more than $7,500, then full coverage auto insurance might be worth the premiums if you can afford it. At a minimum, you should probably have either collision or comprehensive coverage.

When considering when to drop comprehensive and collision coverage, it's typically recommended to drop collision coverage first. That way, you'd still have coverage for damage to your vehicle caused by many different threats other than collisions. However, you should have enough put away in emergency savings to cover a worst-case scenario before you drop either coverage.

How to Save on Comprehensive and Collision Insurance in 2026

There are lots of common car insurance discounts and other ways to save more money on your policy. Follow any of these easy tips below to get more affordable collision and comprehensive insurance this year:

- Bundle your coverage: Buying your homeowners insurance and auto insurance from the same carrier can help you get a bundling discount and earn significant savings on each coverage.

- Raise your deductible: Increasing your policy's deductible by a few hundred dollars can result in much lower premiums.

- Ask about telematics/usage-based programs: Your carrier may offer you a discount for enrolling in their telematics program that tracks your driving behavior and annual mileage.

- Insure multiple vehicles: If you insure more than one car with the same carrier, you can often earn a multi-vehicle discount.

- Ask about garage parking discounts: Many carriers offer these if you keep your vehicle parked in a safe garage while not in use.

- Ask about anti-theft discounts: If your car is equipped with anti-theft devices, you can often earn a discount on your comprehensive coverage.

A local independent insurance agent can also help you learn more about how to save on car insurance in 2026.

FAQs About Comprehensive vs. Collision Insurance

Is hitting a deer comprehensive or collision?

Hitting large animals, including deer, is covered under comprehensive insurance, not collision, even though impact is involved.

Do I need both comprehensive and collision insurance?

In certain cases, yes. Both types of coverage are usually required by auto lenders and lessors for financed and leased vehicles. If you own your car outright, these coverages are optional. However, both are recommended if your vehicle's ACV exceeds 10 times the annual premium amount.

Does comprehensive cover flood damage?

Yes, comprehensive insurance covers flood damage as well as damage from hurricanes, hail, wildfires, and many other natural disasters.

Does collision cover a hit-and-run?

Yes. Collision insurance pays for damage to your car if another driver hits you and flees the scene, regardless of fault. Some states, however, categorize hit-and-run accidents as falling under uninsured motorist coverage instead.

What’s a good deductible for comprehensive and collision?

Most drivers choose a $500 deductible for each coverage. Raising your deductible to $1,000 typically lowers the premium by 10–20%. However, lenders may cap deductibles at $1,000.

Can I have comprehensive without collision?

Yes. Most carriers let drivers carry comprehensive alone, which is common for stored vehicles or older cars where the collision premium exceeds the benefit. However, lenders require both types of coverage on financed and leased vehicles until your loan or lease is paid off.

When should you drop comprehensive and collision?

Apply the 10% rule: drop one or both when the annual premium exceeds 10% of the vehicle’s actual cash value. It's often recommended to drop collision before comprehensive, because the collision premium is typically higher.

An Independent Insurance Agent Can Help You Compare Comprehensive and Collision Insurance

When it comes to finding the right collision or comprehensive car insurance, no one's better equipped to help than a local independent insurance agent. These agents can shop and compare car insurance quotes and policies for you from several local auto insurance companies. They can also help you determine which type of coverage makes the most sense for your unique needs and even file car insurance claims for you down the road.

Sources

https://www.iii.org/article/what-is-covered-by-collision-and-comprehensive-auto-insurance

https://www.iii.org/fact-statistic/facts-statistics-auto-insurance

https://www.insurance.com/auto-insurance/coverage/comprehensive-and-collision-auto-insurance.html

https://www.forbes.com/advisor/car-insurance/average-cost-of-car-insurance/

https://www.experian.com/blogs/ask-experian/comprehensive-vs-collision-insurance/

https://insurify.com/car-insurance/report/

https://www.bankrate.com/insurance/car/average-cost-of-car-insurance/